Inflation Remains a Key Tenant Concern Despite Some Signs of Easing

Monthly inflation pace slows. May CPI data did not show that inflation is solved, but the report offered signs that the most disruptive phase of the price shock may be easing. Headline CPI rose 0.5 percent in May, down from 0.6 percent in April, bringing the annual rate to 4.2 percent. The report also showed pressure stayed concentrated rather than broad-based, as higher energy prices drove much of the increase. Core CPI rose just 0.2 percent month-over-month and 2.9 percent year-over-year, signaling limited spillover into other categories. This contained core reading gives little evidence for near-term Fed rate hikes, barring another major shock. While elevated energy costs may still weigh on household budgets, slower inflation momentum should help preserve consumer spending and tenant activity.

U.S. exports help restrain oil prices. Despite uncertainty over when the Strait of Hormuz will fully reopen, Brent crude has largely remained below $100 per barrel since late May. Record U.S. crude exports have helped cushion the shock, approaching 6 million barrels per day, up from roughly 4 million before the conflict. This added supply represents a durable buffer that should help backfill global markets while Middle Eastern flows remain disrupted. Major importers have also reduced crude purchases and refinery runs, while strategic reserves have provided a shorter-term bridge. An IEA program will make more than 400 million barrels available, including 172 million barrels from the U.S. over about 120 days. Yet reserve releases are temporary, and the U.S. portion could be largely drawn down by mid-August, creating renewed upside risk if the strait remains closed.

Softer goods inflation supports big-box retail. Core goods prices stayed subdued despite tariffs, falling 0.1 percent in May and rising 1.1 percent year-over-year. Fading tariff effects may help offset freight-related price pressure if higher transportation costs begin feeding into goods prices. This could support expansion among goods-handling tenants that can fill big-box spaces, including Home Depot and IKEA, which each plan roughly 10 new U.S. stores in 2026, alongside Tractor Supply’s 100 planned openings. Freight costs remain a key risk. Drewry’s World Container Index jumped 23 percent between May 28 and June 4, reflecting earlier peak-season ordering and fuel-related shipping costs. Import-heavy retailers, distributors, and logistics users could face added pressure if shipping costs stay elevated.

Crop inputs shape restaurant risk. Food prices remained soft, as the index rose just 0.2 percent in May and 3.1 percent year-over-year. Higher fertilizer prices could still pose a lagged risk as planting-season expenses flow through crop-linked foods. This may create uneven restaurant exposure. Bakeries, pizza concepts, salad chains, and sandwich shops face more direct risk from wheat, produce, oils, and other crop inputs. Beverage-heavy concepts may be better insulated, while meat- and dairy-focused operators face slower feed-cost pass-through and separate livestock-cycle pressure. Still, tenant performance will depend on brand strength, value perception, and operating discipline.

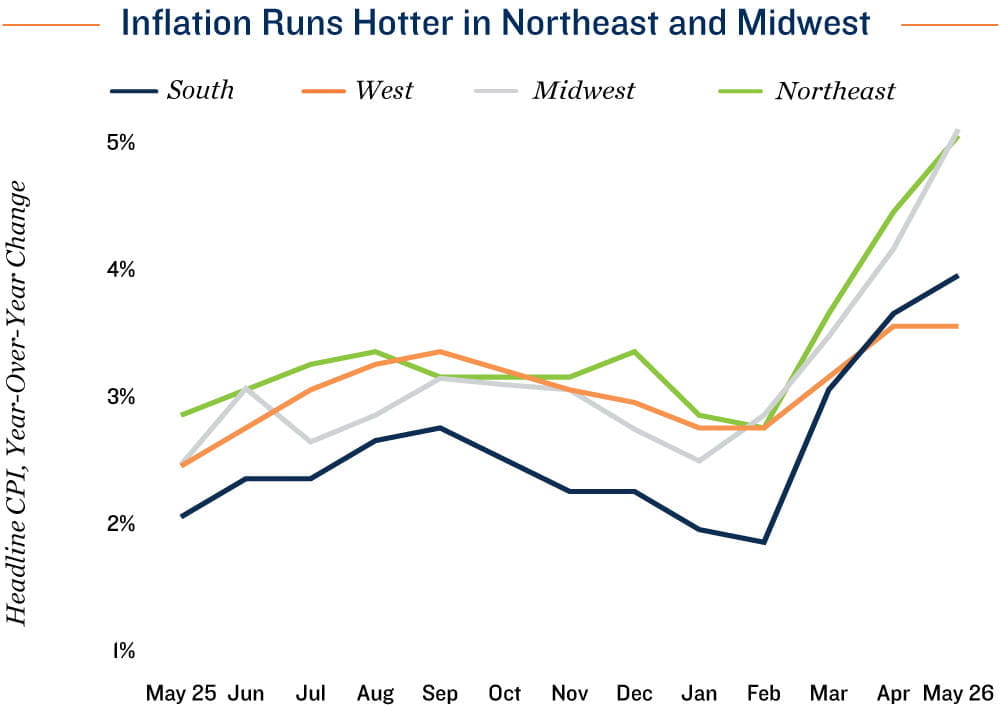

Regional inflation paths diverge. CPI rose 5.0 percent year-over-year in both the Northeast and Midwest, while staying below 4 percent in the South and West. Energy costs were a key driver, as colder-weather markets and regions farther from major refining hubs are more sensitive to oil price swings. Rent inflation was also firmer in several older, supply-constrained metros, while stronger apartment construction in the South and West has slowed rent growth and helped ease rent burdens. This could preserve household spending in lower-inflation regions, supporting broader retail and service-sector demand.

4.2%

|

2.9%

|

|

Increase in Headline

CPI Year-Over-Year

|

Increase in Core CPI

Year-Over-Year

|

Sources: Marcus & Millichap Research Services; Bureau of Labor Statistics; Drewry; Energy

Information Administration; Federal Reserve