Research Brief

Canada Monetary Policy

June 2026

Higher-for-Longer Rate Environment

Curbing CRE Investment Momentum

Central bank keeps cautious stance amid elevated inflation risks. The Bank of Canada held the overnight rate at 2.25 per cent, as policymakers continued balancing a weak domestic economy against persistent inflationary pressures amid elevated energy prices, geopolitical conflict, and ongoing trade uncertainty. While Canada’s economy contracted modestly in the first quarter and labour market conditions remain soft overall, recent data suggests growth may resume in the second quarter. At the same time, rising oil prices linked to the conflict in the Middle East, coupled with tariff uncertainty and global supply chain disruptions, are expected to keep headline inflation elevated in the near term. As a result, the Bank reiterated its commitment to maintaining price stability and signalled that it remains prepared to respond should inflationary pressures become more persistent.

Central bank balancing many factors. While softer economic conditions would normally support additional easing, persistent inflation risks continue to limit the Bank of Canada’s flexibility. As a result, the monetary authorities’ rate outlook is becoming increasingly challenging. While many forecasters — including four of Canada’s five largest banks — continue to call for the overnight rate to remain on hold at 2.25 per cent through the remainder of the year, money markets are starting to price in one rate hike before year-end. That said, these inflationary pressures remain highly fluid, meaning the policy outlook could shift relatively quickly should geopolitical tensions ease and price pressures moderate.

Commercial Real Estate Outlook

Signs of economic stabilization emerging. Canada’s economy contracted in both the fourth quarter of 2025 and first quarter of 2026, marking the first consecutive quarterly decline since the pandemic slowdown, as elevated borrowing costs, weaker population growth, and ongoing trade uncertainty tempered activity. Even so, stronger energy exports, improving manufacturing activity, and modest gains in real GDP per capita suggest underlying conditions remain somewhat firmer than headline figures imply, supporting expectations for a gradual rebound over the second half of the year. This mixed economic backdrop is also contributing to increased volatility in longer-term bond yields. While slower growth and softer demand should help prevent a significant upward surge in yields, ongoing inflation concerns tied to energy prices, tariffs, and elevated government deficits are still expected to keep some upward pressure on yields.

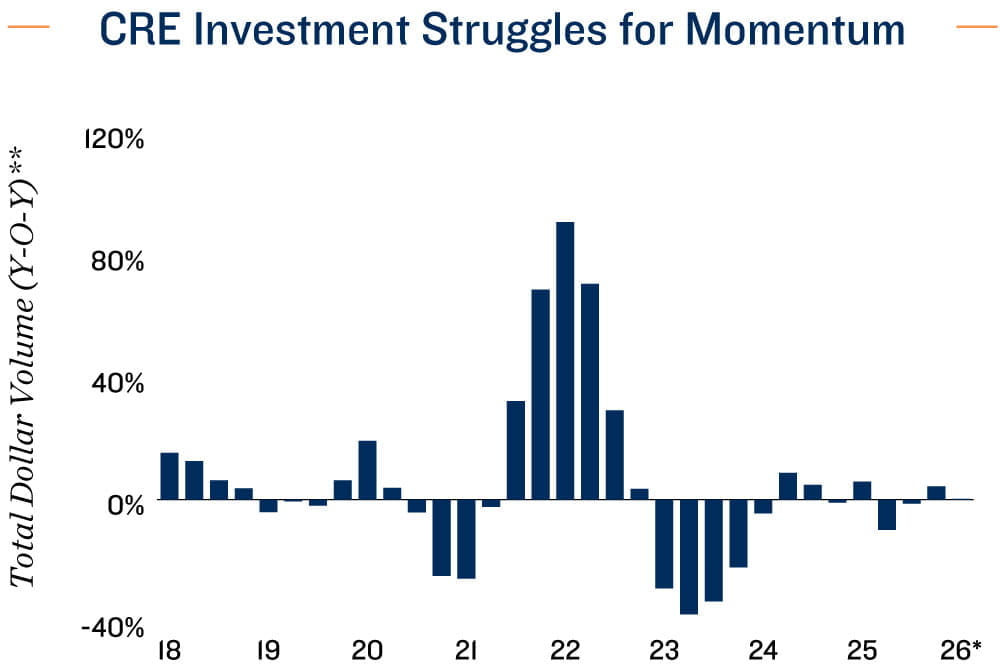

Real estate investment struggles for direction. After rebounding sharply in 2023, sales momentum slowed materially over the past year as volatile bond yields, underwriting challenges, trade tensions, and geopolitical risks curbed improving investor sentiment. That said, an improving economic backdrop, Canada’s relative stability, commercial real estate’s defensive characteristics, and a largely completed asset repricing cycle should gradually support sales activity. Investor demand continues to favour defensive, income-producing assets with stable cash flows. At the same time, dwindling supply pressures, improving demand, and favourable pricing are pulling some investors back toward high-quality office.

* Through 1Q ** Trailing 12-month total

Sources: Marcus & Millichap Research Services; Altus Data Solutions; Capital Economics; CIBC;

CMHC; CoStar Group, Inc.; Oxford Economics; RBC; Scotiabank; Statistics Canada; TD

TO READ THE FULL ARTICLE