Research Brief

Canada GDP

June 2026

Commercial Property Sector Navigating Demographic Shifts and Economic Stall

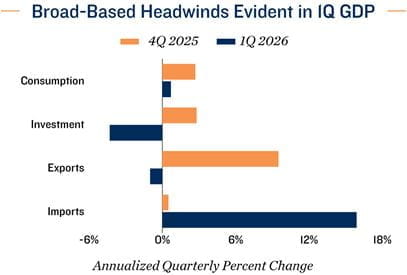

GDP ended first quarter on a soft note. Canada’s economy remained flat in the first quarter of 2026, contracting slightly by 0.1 per cent on an annualized basis following a 1.0 per cent decline in the previous quarter. This second consecutive quarterly contraction was driven by slower consumption growth, declining investment, and weaker net exports amid surging imports. Part of the decline reflects temporary factors, including a winter-related production halt in the auto sector that has since reversed. More recently, exports have likely strengthened since April alongside a sharp rise in global oil prices. As a result, GDP is expected to rebound in the second quarter. In addition, despite the weak headline figure, real GDP per capita rose 0.9 per cent, suggesting underlying conditions were stronger on a per-person basis amid muted population growth.

BoC stays put amid soft growth backdrop. The advance estimate for April GDP points to a 0.4 per cent monthly increase, supported by stronger energy production and manufacturing activity. This gain puts second-quarter growth on track for roughly a 2.0 per cent annualized pace, bringing an end to the consecutive quarter decline. Overall, GDP is estimated to have expanded by 1.0 per cent in the first half of the year, undershooting the Bank of Canada’s 1.5 per cent forecast. While the Bank has signaled its readiness to respond if the ongoing Middle East conflict leads to persistent inflation, the broader soft growth backdrop should help contain price pressures. As such, the Bank is expected to keep rates on hold through year-end.

Commercial Real Estate Outlook

Consumer sectors facing demographic headwinds. The contrast between a decline in total GDP and an increase in output per capita underscores the ongoing demographic shift in Canada. Since peaking in the third quarter of last year, the population has declined by 0.4 per cent by the first quarter of this year — a trend expected to persist through at least next year amid tighter immigration policies. Muted population growth is set to moderate demand across consumer-driven sectors. In multifamily, weaker household formation should ease rent growth and lift vacancy modestly, particularly in markets that recently absorbed strong immigration inflows. In retail, softer population gains are likely to temper foot traffic, especially in suburban and expansion submarkets, while vacancy rates edge up slightly from current lows as leasing normalizes.

Rising business investment a new industrial demand driver. One bright spot in the first-quarter GDP report is an acceleration in investment growth in machinery and equipment, as well as intellectual property products — rising 10 per cent and 14 per cent, respectively. This rebound in business investment signals the next phase of demand drivers for the industrial sector, particularly across manufacturing, logistics, and AI-related digital infrastructure. As firms expand capacity and modernize operations, leasing activity for distribution and specialized facilities, including data centres, is likely to firm, helping stabilize occupancy levels and support more balanced vacancy dynamics despite broader economic softness.

Sources: Marcus & Millichap Research Services; Capital Economics; CoStar Group, Inc; Oxford

Economics; Statistics Canada

TO READ THE FULL ARTICLE