Research Brief

Canada Employment

July 2026

Industrial Fundamentals Strengthen

as Labour Market Gradually Improves

Canada’s labour market continued to stabilize. Employment increased by 18,200 positions in June, following May’s much stronger gain, while the unemployment rate edged down 10 basis points to 6.5 per cent. However, the composition of hiring was less encouraging, as nearly all of the increase came from part-time employment and younger workers, likely reflecting seasonal hiring and stronger demand tied to the FIFA World Cup. This was reflected in the concentration of job gains in wholesale and retail trade, as well as in accommodation and food services. At the same time, goods-producing employment declined amid continued weakness in manufacturing and construction. Although wage growth improved to 3.3 per cent year-over-year, the overall results point to a labour market that is stabilizing rather than materially tightening.

Bank of Canada likely to remain on the sidelines. Labour market conditions have generally begun to improve in recent months, and the conflict in the Middle East continues to create periodic inflation risks through energy markets. However, policymakers are more likely to continue to consider the downside risks to economic growth stemming from ongoing trade uncertainty. Although inflation has remained broadly contained and employment conditions have become more resilient, the Bank is likely to remain on the sidelines until there is greater clarity around the economic effects of tariffs and global trade policy. Barring a material deterioration in growth or a renewed surge in inflation amid energy price concerns, the overnight rate is expected to remain unchanged at 2.25 per cent over the coming months.

Commercial Real Estate Outlook

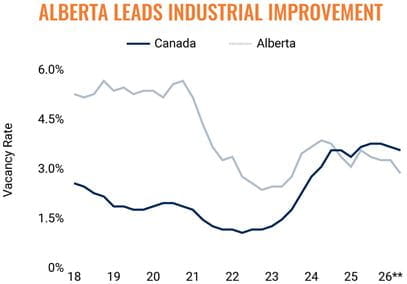

Industrial demand improving despite some headwinds. Trade uncertainty and tariffs on several key goods-producing industries contributed to a 16,800-position decline in manufacturing employment in June, leaving total employment in the sector down 1.1 per cent year over year. Nevertheless, industrial net absorption has remained positive for four consecutive quarters as of June, helping national vacancy fall by 20 basis points from its 2025 peak to 3.5 per cent. Leasing demand has been supported by a resilient consumer and continued requirements from distribution and warehousing users. Meanwhile, some businesses are also adjusting inventories and supply chains in response to trade disruptions. Combined with a sharply reduced construction pipeline, these trends are gradually improving market conditions.

Alberta’s outperformance improves industrial fundamentals. Employment in Alberta rose 3.0 per cent year-over-year in June — the fastest pace nationwide. Higher energy prices following the conflict in the Middle East, the province’s growth as a lower cost distribution hub, and a more supportive policy environment for energy infrastructure investment have reinforced economic momentum. These trends have also supported Alberta’s industrial market, with net absorption remaining largely positive since early 2024. Combined with measured new supply, vacancy has declined by roughly 100 basis points over that period to 2.8 per cent as of June, well below the national average.

* Forecast; ** Preliminary estimate through 2Q | Sources: Altus Data Solutions; Capital

Economics; CoStar Group, Inc.; Oxford Economics; Statistics Canada

TO READ THE FULL ARTICLE