Research Brief

Canada Business Outlook

July 2026

Industrial Demand Recovery Remains

Intact Amid Steady Corporate Sentiment

Business confidence held steady despite uncertainty. The Bank of Canada’s second-quarter Business Outlook Survey suggests that business confidence remained relatively resilient amid external headwinds, with overall activity softening only modestly. Higher oil prices improved sentiment in the energy sector, partly offsetting weaker conditions across non-energy industries. Meanwhile, the resulting inflationary pressures appear to have been short-lived. Although two-year inflation expectations rose to 3.2 per cent in the survey, the monthly Business Leaders’ Pulse survey indicates that short-term price pressures eased in June, with longer-term expectations remaining well anchored. Although events in the Middle East remain fluid, somewhat dating the outlook survey, the results provide a snapshot of business sentiment amid heightened geopolitical uncertainty.

Investment and export conditions continued to improve. While overall business activity softened, investment intentions strengthened from already robust levels at the beginning of the year, driven by a growing focus on productivity-enhancing initiatives such as equipment upgrades and AI adoption. Another bright spot was improving sentiment among exporters. Beyond the cyclical fluctuations associated with oil exports, the effects of lingering trade tensions continued to fade. Fewer businesses reported that U.S. customers were delaying orders because of uncertainty surrounding trade policy changes. At the same time, some firms responded by adapting their operations, adjusting supply chains, or diversifying into new industries to reduce tariff exposure.

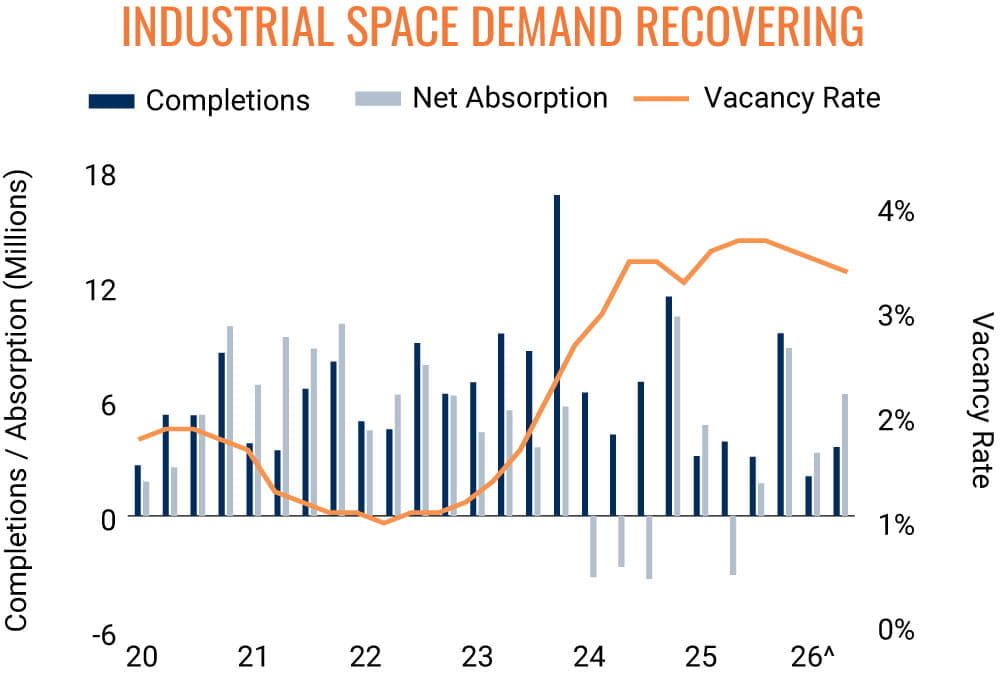

Commercial Real Estate Outlook

USMCA setback unlikely to deter industrial recovery. With the U.S. opting not to renew the USMCA during the 2026 review, the agreement will now be subject to annual reviews and is set to expire in 2036 unless a future extension is reached. However, this development appears unlikely to meaningfully disrupt trade or investment activity in the near term. Despite the uncertainty surrounding the trade pact, industrial space demand finished the first half of the year on a strong footing, with net absorption nearing 10 million square feet nationwide and vacancy falling to 3.4 per cent. This momentum is expected to continue through year-end as the risk of renewed trade tensions remains low. However, any longer-term deterioration in trade conditions would likely weaken business investment and trade flows, limiting demand for industrial space over time

Corporate and international demand to lead hotel gains. The Consumer Expectations Survey echoes the findings of the Business Outlook Survey, showing that long-term inflation expectations remain stable. Nevertheless, the rise in gas prices weighed on nearterm spending plans, with consumers expecting higher inflation, indicating they would reduce discretionary spending such as dining out and travel. This aligns with the outlook for the hotel sector, where demand growth this year is expected to be driven primarily by business travel and inbound tourism. In contrast, domestic leisure travel remains constrained by economic headwinds.

* Percentage of firms reporting positive sentiment minus the percentage reporting negative sentiment;

** Through 2Q; ^ Preliminary estimates through 2Q | Sources: Altus Data Solutions;

Bank of Canada; Capital Economics; Oxford Economics

TO READ THE FULL ARTICLE