Research Brief

Hospitality Outlook

June 2026

Supply Discipline Helps Hotel Sector

Navigate Demand Pressures

Economic headwinds challenge travel demand. Rising vacation-related expenses have dampened consumer confidence heading into this year's summer travel season.

- Elevated energy costs, airfares up 21 percent annually, soft employment conditions, and record-low consumer sentiment are weighing on discretionary travel demand this summer.

- Rising gas prices are significantly altering summer travel behavior, with 70 percent of consumers reporting changes to vacation plans.

- Consumer sentiment has fallen to a record low, potentially signaling near-term caution in discretionary spending decisions.

- The share of consumers planning to stay in paid lodging has fallen to 45 percent, the lowest level in six years.

- Summer travel pullbacks are income-skewed, with higher-earning households showing only modest declines, while lower-income households are cutting travel plans more sharply.

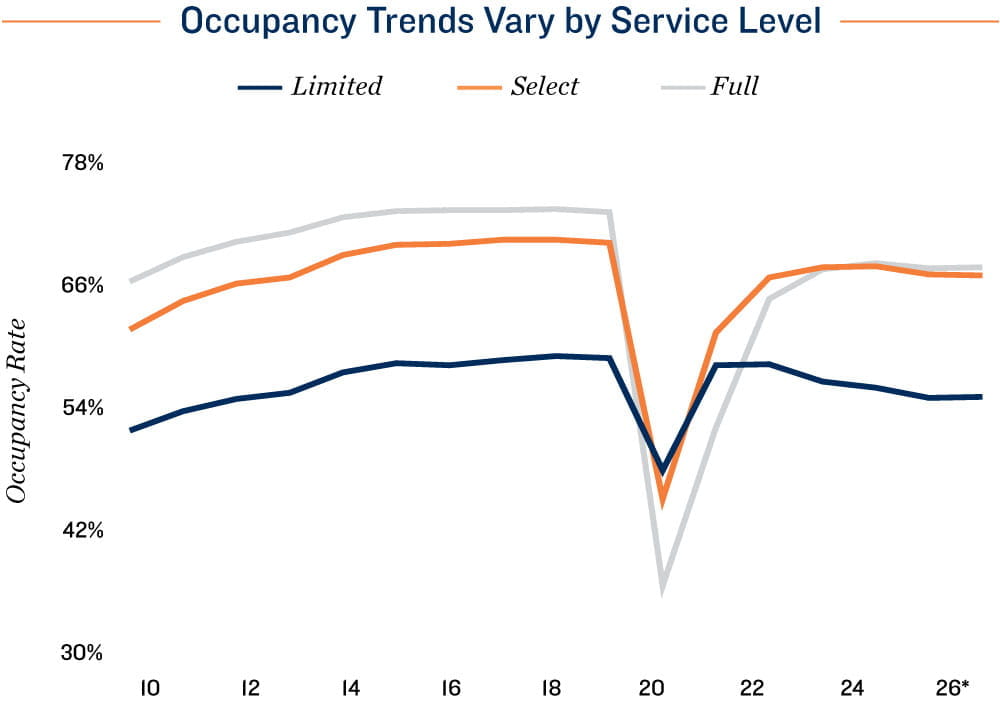

Segment performance diverges. Occupancy and booking trends vary by hotel service level, with demand softness concentrated in lower tiers. Less supply growth also tempers downside risk.

- Limited-service hotels are seeing the most softness in demand, reflecting greater exposure to lower-income consumers.

- Limited-service hotel occupancy has trended lower since 2019, declining from a peak above 58 percent to the low-54 percent range by late 2025, and remaining there as of May 2026.

- Demand for select-service hotels has remained relatively stable, with total room nights sold largely unchanged since 2023.

- As of May 2026, select-service room occupancy is down only 1.0 percent from the 2019 peak, underscoring resilience in that segment.

- Performance varies by chain scale, with occupancy softening in economy and midscale hotels while the upscale and luxury segments show greater durability.

- New hotel supply growth remains muted, with additions down 34 percent from 2019 levels due to elevated construction, financing, materials, and labor costs, which help limit downside risk to fundamentals.

Capital markets regain some traction. With deal flow improving, pricing stable, and supply risk constrained, the hospitality investment outlook remains cautiously positive and steady despite near-term demand headwinds.

- Transaction activity has been gradually rising over the trailing 12 months ended March, with deal volume up 19 percent from the 2024 cyclical trough and roughly in line with 2016 levels.

- Pricing has remained stable since 2023, averaging about $113,000 per key with cap rates near 8.7 percent.

- Delinquency rates remain modest and well below the peaks seen during the global financial crisis of 2007-2009 and the pandemic.

- Investment performance is increasingly bifurcated, with upper-tier hotels outperforming lower-cost segments.

- Hotels offer relative inflation resistance, as daily room rate pricing allows for faster revenue adjustments.

- Looking beyond near-term headwinds, demand drivers could strengthen as economic momentum improves while limited new supply supports a constructive long-term outlook.

* Forecast

Sources: Marcus & Millichap Research Services; American Automobile Association; Bank of

America; Bureau of Economic Analysis; Bureau of Labor Statistics; CoStar Group, Inc.; Deloitte;

Federal Reserve; Real Capital Analytics; Trepp; University of Michigan;

U.S. Energy Information Administration

TO READ THE FULL ARTICLE