Research Brief

Canada Retail Sales

June 2026

Signs of Stabilization Emerging Across Consumer Spending and CRE

Households remain cautious. Retail sales increased 0.5 per cent month-over-month, driven largely by a 5.1 per cent gain at gasoline stations and fuel vendors. Higher prices stemming from the conflict in the Middle East were the main driver of the increase in receipts. Sales also rose at motor vehicle dealers, building material and garden equipment stores, and furniture and appliance retailers, with the latter two potentially reflecting improved housing market activity. These gains were partially offset by weaker spending on food and beverages, general merchandise, and sporting goods. After adjusting for inflation, retail sales volumes were unchanged, indicating that underlying consumer demand remained relatively soft despite the headline increase amid lingering uncertainties.

Discretionary spending remains uneven. Mixed consumer spending patterns persisted across retail categories in March, with higher fuel costs and ongoing affordability pressures increasingly weighing on discretionary purchases. Sales at building material and garden equipment stores fell 2.9 per cent during the month, while general merchandise retailers also posted a decline. At the same time, spending on essential-based categories remained comparatively resilient, with food and beverage retailers recording a 0.5 per cent increase, led by stronger grocery sales. Preliminary estimates suggest retail sales rose another 0.6 per cent in April, though much of that increase was likely again tied to higher gasoline prices rather than stronger underlying consumption. As a result, household spending momentum appears to be slowing heading into the second quarter.

Commercial Real Estate Outlook

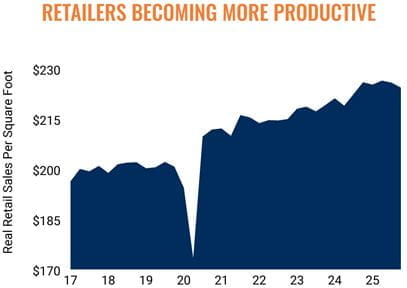

Retail fundamentals remain sound. Many retailers have shifted focus from aggressive expansion toward maximizing sales within existing locations, resulting in higher sales productivity and stronger profitability. Under normal circumstances, this trend could reduce space demand and put upward pressure on vacancy rates. However, a prolonged period of limited retail construction, driven by elevated development and financing costs, has constrained new supply across most major markets. As a result, available space remains scarce, supporting rent growth despite a more moderate pace of improvement in consumer spending and economic activity.

E-commerce a tailwind for industrial real estate. Although online sales fell 1.2 per cent monthly in April, they remained 0.8 per cent higher than a year earlier. E-commerce also represented 7 per cent of total retail sales, well above the pre-pandemic average of 3 per cent, highlighting the structural shift toward online shopping. At the same time, shifting supply chain strategies amid fluid trade dynamics are supporting renewed demand for industrial space. Preliminary second-quarter data indicate net absorption is on track to exceed first-quarter levels, extending a recovery that has been underway since late 2024. Together with moderating supply-side pressures, fundamentals are stabilizing, with Canada’s industrial vacancy rate declining to 3.6 per cent in the second quarter, down 10 basis points from its peak at the end of 2025.

* Through April | Sources: Altus Data Solutions; Capital Economics; CoStar Group, Inc.; Oxford Economics; Statistics Canada

TO READ THE FULL ARTICLE