Research Brief

Retail Outlook

May 2026

Despite Economic Pressures, Supportive

Retail Tailwinds Help Fuel Investment

Consumers display resilience amid crosswinds. While inflation, debt, and sentiment have deteriorated, wage growth and strong household balance sheets support spending capacity.

- U.S. consumption has remained resilient over the past year, with inflation-adjusted retail sales continuing to rise despite multiple economic headwinds.

- Job creation through the first four months of 2026 averaged roughly 76,000 positions per month, modest by historical standards but stronger than 2025's monthly pace of about 10,000.

- Consumer sentiment has fallen to a record low, potentially signaling near-term caution in discretionary spending decisions.

- Meanwhile, inflation pressures have ignited, with CPI climbing 50 basis points to 3.8 percent in April, the highest level since 2023, while household debt reached a record $18.8 trillion.

- However, strong wage growth over the past three years has supported household balance sheets, keeping debt as a share of income at its lowest level in more than 15 years.

- Household savings, including money market funds, rose 3.4 percent in the past year to a record high, suggesting consumers retain meaningful purchasing power if they choose to spend.

Opposing multi-tenant trends. Despite rising vacancy and cautious retailer expansion, limited new supply and elevated retail sales support multi-tenant rent growth.

- Total retail sales increased 4.0 percent last year and rose approximately 0.5 percent on an inflation-adjusted basis.

- Growth has been led by e-commerce, with non-store retail sales up 10.1 percent year-over-year, while brick-and-mortar sales also advanced, rising 2.4 percent over the past year.

- Multi-tenant vacancy rose modestly in the first quarter to 6.0 percent amid negative absorption, reflecting retailer caution.

- Still, multi-tenant construction activity is at its lowest level since 2011, which should reduce new supply risk.

- As a result, multi-tenant rents have recently edged higher, rising 1.1 percent in the 12 months trailing March.

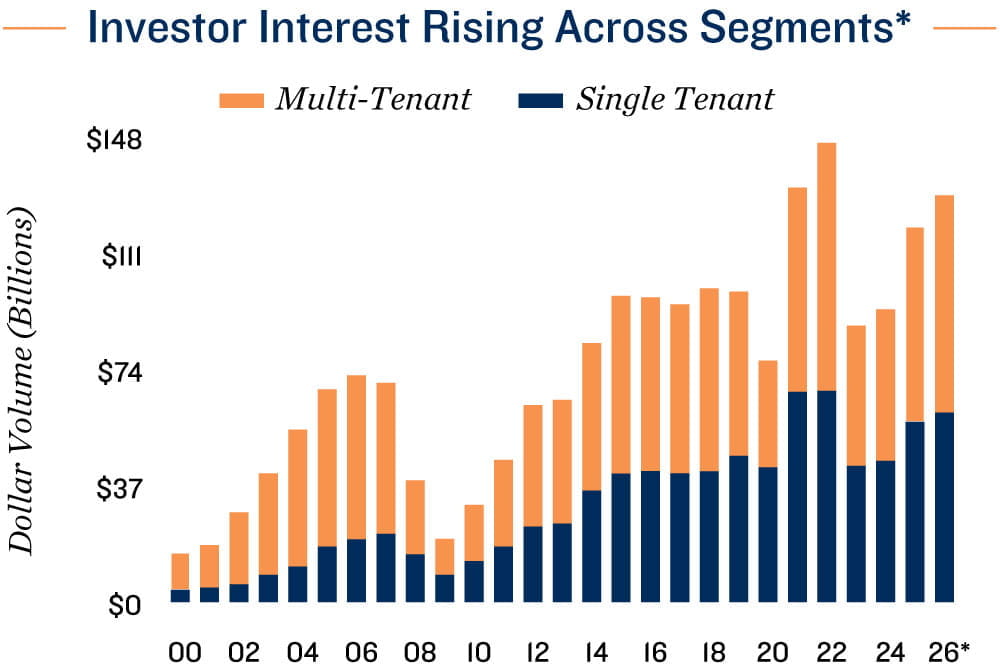

Wide vacancy dispersion across single-tenant formats. Segment fundamentals remain generally stable, while investor interest across both single and multi-tenant remains active.

- Single-tenant retail vacancy increased modestly in the first quarter of 2026, rising 10 basis points to 4.6 percent, with rent growth of 1.1 percent year-over-year.

- Vacancy varied by subsector, with department stores at 6.4 percent and drug stores at 6.0 percent, compared with restaurants at 3.5 percent and grocery stores at 2.6 percent.

- Quick-service restaurants posted a 1.5 percent vacancy rate, while convenience stores recorded the lowest rate among single-tenant subsectors at just 1.0 percent.

- Retail investment remains active, with trailing 12-month multitenant transaction volume roughly in line with 2021 levels and only 9.6 percent below the 2022 peak, while cap rates averaged approximately 7.3 percent.

- Single-tenant investment has also been robust, with deal flow over the last four quarters just 4.2 percent below the 2021 peak, while cap rates averaged near 6.6 percent but varied by tenant credit and lease term.

*Sales greater than $1 million, **Trailing 12 months through March

Sources: Marcus & Millichap Research Services; Bureau of Economic Analysis; Bureau of Labor

Statistics; CoStar Group, Inc.; Federal Deposit Insurance Corporation; Federal Reserve; Federal

Reserve Bank of Atlanta; Federal Reserve Bank of New York; Moody's Analytics; Mortgage Bankers

Association; Office of Financial Research; Real Capital Analytics; RealPage Inc.; RetailStat;

University of Michigan; U.S. Census Bureau

TO READ THE FULL ARTICLE