Research Brief

Canada Retail Sales

May 2026

Experiential and Essential Retail Outperforming

Amid Uncertain Macro Backdrop

Higher gasoline prices weigh on retail sales volumes. Canada’s retail sector lost momentum in March, as rising gasoline prices and softer discretionary demand weighed on household spending activity. While headline retail sales increased 0.9 per cent to $72.7 billion, much of the gain was driven by a 12.4 per cent surge in gasoline station sales following the supply shock tied to the ongoing Middle East conflict. In volume terms retail sales declined 0.7 per cent, suggesting consumers purchased fewer goods despite spending more in nominal figures. Excluding gasoline stations and motor vehicle dealers, core retail sales edged down 0.1 per cent, reinforcing signs that underlying consumer demand softened during the month despite retail receipts posting a seventh consecutive quarterly increase overall.

Discretionary spending remains uneven. Mixed consumer spending patterns persisted across retail categories in March, with higher fuel costs and ongoing affordability pressures increasingly weighing on discretionary purchases. Sales at building material and garden equipment stores fell 2.9 per cent during the month, while general merchandise retailers also posted a decline. At the same time, spending on essential-based categories remained comparatively resilient, with food and beverage retailers recording a 0.5 per cent increase, led by stronger grocery sales. Preliminary estimates suggest retail sales rose another 0.6 per cent in April, though much of that increase was likely again tied to higher gasoline prices rather than stronger underlying consumption. As a result, household spending momentum appears to be slowing heading into the second quarter.

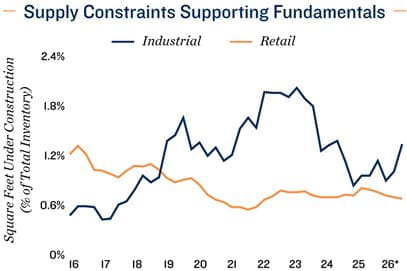

Commercial Real Estate Outlook

Consumers remain in a more defensive position. Essential categories continue to drive the broader retail landscape. Consumers are becoming more cautious with their spending, increasingly focusing on necessities rather than optional goods. This trend is likely to persist in the near term, particularly as higher gasoline prices — driven by the ongoing Middle East conflict — place added pressure on household budgets. This will limit the upside for discretionary retail segments and reinforce a more subdued consumption outlook. As a result, grocery-anchored, essential-based retail should remain a preferred investment option.

Necessity and experiential retail outperform. Consumer trends continue to favour defensive and experience-oriented retail formats within commercial real estate. Grocery-anchored centres and service-based retail assets remain well positioned as consumers continue prioritizing essential purchases amid elevated living costs. At the same time, experiential retail categories tied to dining, entertainment and personal services continue to benefit from consumers allocating a greater share of spending toward experiences rather than larger discretionary goods purchases. This trend is helping support foot traffic across mixed-use retail nodes and urban high streets, particularly in major metropolitan markets where demand for food services and entertainment-oriented space remains relatively healthy

* Preliminary estimates through 2Q

Sources: Marcus & Millichap Research Services; Altus Data Solutions; Capital Economics; CoStar

Group, Inc.; Oxford Economics; Statistics Canada

TO READ THE FULL ARTICLE