Research Brief

Canada Inflation

May 2026

Inflation Volatility Highlights Shift

Toward Essential-Based Retail Properties

Middle East conflict pushes headline inflation higher. Canada’s annual inflation rate accelerated 40 basis points to 2.8 per cent in April, driven by a roughly 7 per cent increase in gasoline prices amid ongoing conflict in the Middle East. Even so, the reading came in below consensus expectations of 3 per cent, suggesting that broader inflationary pressures remain relatively contained. Food prices were also softer than anticipated and remained effectively unchanged on a monthly basis, helping offset some of the energy-driven gains. Outside of gasoline, inflation across several discretionary categories remained subdued, reflecting softer consumer demand and ongoing labour market weakness.

Muted core inflation supports rate stability. Underlying inflation measures continue to point toward easing price pressures and support a more stable rate outlook. The Bank of Canada’s preferred core inflation measures — CPI-trim and CPI-median — both increased at a pace broadly consistent with the central bank’s inflation target in April. While the average three-month annualized rate edged up slightly to 1.8 per cent, the average annual rate slowed to 2.1 per cent, marking its lowest level since early 2021. Combined with softer consumer demand and a gradually cooling labour market, the latest inflation data should reduce pressure on the Bank of Canada to raise interest rates further in the near term, despite lingering energy-related risks. As a result, the overnight rate is still expected to remain relatively stable over the coming quarters, helping preserve improving financing conditions across commercial real estate markets.

Commercial Real Estate Outlook

Discretionary pullback weighing on retail property fundamentals. While Canada’s retail sector remains healthy overall — with vacancy still forecast to stay below 3 per cent over the coming year — conditions have moderated from the exceptionally tight levels seen in recent years. Vacancy has risen roughly 100 basis points from its 2024 low, while rent growth has slowed to about 1 per cent from the 4 per cent range recorded through much of the past two years. Slowing population growth tied to tighter immigration policy, combined with geopolitical uncertainty, is beginning to pressure consumer confidence and discretionary spending, consistent with softer inflation across several nonessential categories. In contrast, grocery-anchored and other essential-based retail formats continue to post tight conditions and stronger rent growth, reinforcing their position as one of the sector’s most defensive investment opportunities.

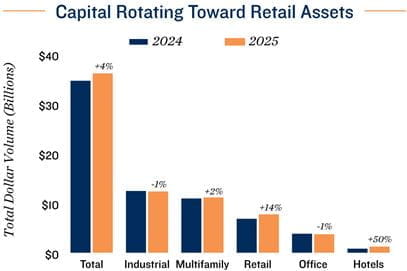

Investor capital shifted towards retail. Preliminary first-quarter data suggest real estate investment generally held up through early 2026, even amid interest rate volatility and heightened uncertainty tied to the Middle East conflict in March. That said, results remain incomplete due to reporting delays in Alberta. More broadly, 2025 transaction trends highlight how retail has reemerged as a preferred investment. Total retail investment volume jumped 14 per cent last year, marking one of the strongest gains among major commercial property types. Notably, the increase was driven entirely by a 28 per cent rise in sales exceeding $20 million, further reinforcing investor preference for larger-scale, grocery-anchored neighbourhood assets.

* Through April ** Forecast

Sources: Marcus & Millichap Research Services; Altus Data Solutions; Capital Economics; CoStar

Group, Inc.; CREA; Oxford Economics; Statistics Canada

TO READ THE FULL ARTICLE