Research Brief

Canada Industrial

May 2026

Capital Reenters Industrial Sector as Manufacturing Benefits from Energy Cycle

Production rose on strength in energy and transportation. Driven by a surge in petroleum and coal product sales, manufacturing sales rose by 3.0 per cent in March, reaching their highest level since January 2025. The escalation of the Middle East conflict led to a 27.4 per cent increase in energy and petroleum prices, pushing total sales in this sector to their highest level since September 2023. The transportation equipment sector also continued to record gains. Production ramped up across several motor vehicle manufacturing plants, while the aerospace segment benefited from AirAsia’s order for 150 A220 aircraft. In price-adjusted terms, total manufacturing shipments increased 1.0 per cent, largely supported by a sharp expansion in motor vehicle production, which jumped 15 per cent.

Elevated oil prices to drive energy-led manufacturing gains. As oil prices remained elevated through April, sales of petroleum and coal products are likely to continue rising into the early summer months, providing further support to manufacturing sales. However, it is noteworthy that in March, while nominal energy sales increased by 23 per cent, real sales declined by 3.5 per cent. This divergence suggests that recent gains have been largely price-driven rather than reflecting stronger underlying demand. Elevated oil prices have likely prompted some households to cut back on gasoline consumption — a trend also evident in the travel industry, as some airlines reduce flights amid oil price volatility, weighing on overall real demand for petroleum products.

Manufacturing ramp-up strengthens industrial outlook. The March increase in new orders, unfilled orders, and the capacity utilization rate points to a strengthening near-term outlook for the industrial sector. Rising new orders signal improving demand, while the buildup in unfilled orders suggests that production pipelines are becoming more robust, providing manufacturers with greater visibility into future output. At the same time, the notable increase in capacity utilization indicates that existing facilities are being used more intensively, reflecting tighter operating conditions. Together, these trends imply that production activity could continue to build momentum in the near term and may even prompt selective capacity expansion or capital investment if sustained, particularly in sectors already experiencing supply-side constraints.

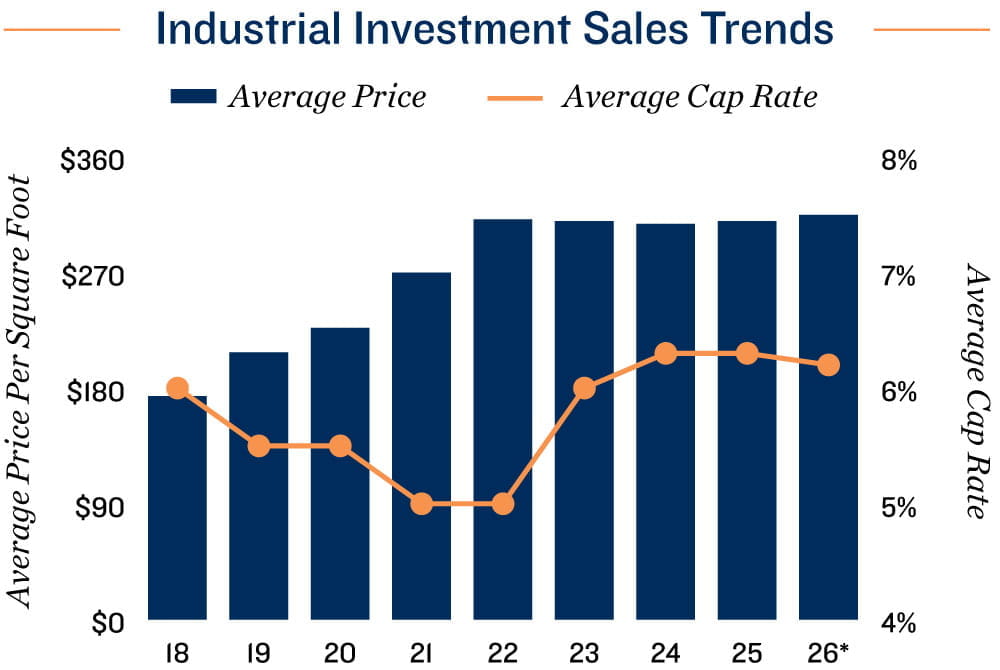

Industrial sales show renewed investor interest. In some trade-dependent metros, including Toronto and Montreal, investment activity rose year-over-year in the first quarter after a subdued 2025. Driven by medium- to large-sized deals, this increase suggests that investor appetite for higher-quality assets is returning. Nationally, cap rates also inched lower alongside a modest uptick in the average sale price, indicating that industrial assets are being perceived as less risky amid stabilizing market conditions. If sustained, this could support further capital reallocation into the sector, particularly as investors gain greater clarity on long-term trade conditions.

Trailing 12 months through 1Q

Sources: Marcus & Millichap Research Services; Altus Data Solutions; Capital Economics; CoStar

Group, Inc.; Oxford Economics; Statistics Canada

TO READ THE FULL ARTICLE