Research Brief

Canada Employment

May 2026

Labour Market Weakness Clouds

Near-Term Housing Outlook

Job creation struggling for momentum. Canada’s labour market continued to weaken in April, with employment declining by 17,700 positions and bringing total job losses this year to nearly 80,000. Meanwhile, the unemployment rate rose 20 basis points to 6.9 per cent — the highest level in six months — reinforcing signs that hiring conditions are poor. Losses were concentrated in cyclical industries, including construction, transportation, and retail trade. Employment in the oil and gas sector also reversed, following a temporary boost tied to higher energy prices in March. More broadly, elevated gasoline costs, trade uncertainty, and weaker consumer confidence appear to be weighing on discretionary spending and business hiring. While the unemployment rate may improve amid muted labour force growth, hiring could soften further over the near term as economic uncertainty continues to pressure employer confidence.

Soft labour print supports rate hold. Ongoing USMCA uncertainty, heightened geopolitical tensions in the Middle East, and firmer GDP growth in February have all contributed to speculation that the Bank of Canada may need to keep rates elevated for longer. Futures markets are even pricing in the possibility of a rate hike. That said, underlying economic conditions are mixed. Labour market momentum continues to soften, housing activity remains subdued, and wage growth has generally stabilized despite the recent increase. As a result, policymakers are still likely to remain cautious, with weaker employment conditions and the upcoming USMCA review expected to keep the Bank of Canada on the sidelines through the remainder of 2026.

Commercial Real Estate Outlook

Ownership challenges maintain rental demand. Softening labour market conditions are beginning to create additional pressure across Canada’s housing market. Historically, weaker employment conditions and elevated borrowing costs have increased financial strain for homeowners, with mortgage arrears largely trending on the same path as rising unemployment. These affordability and financing challenges in the ownership market are likely to keep or push more households to the rental sector for longer, supporting multifamily demand. While tighter immigration, elevated supply growth, and softer labour market conditions are creating near-term softness in the apartment sector, the longer-term outlook continues to remain favourable. Decades of underbuilding, persistent ownership challenges, and population growth returning closer to long-run averages by 2028 should continue supporting multifamily fundamentals over time.

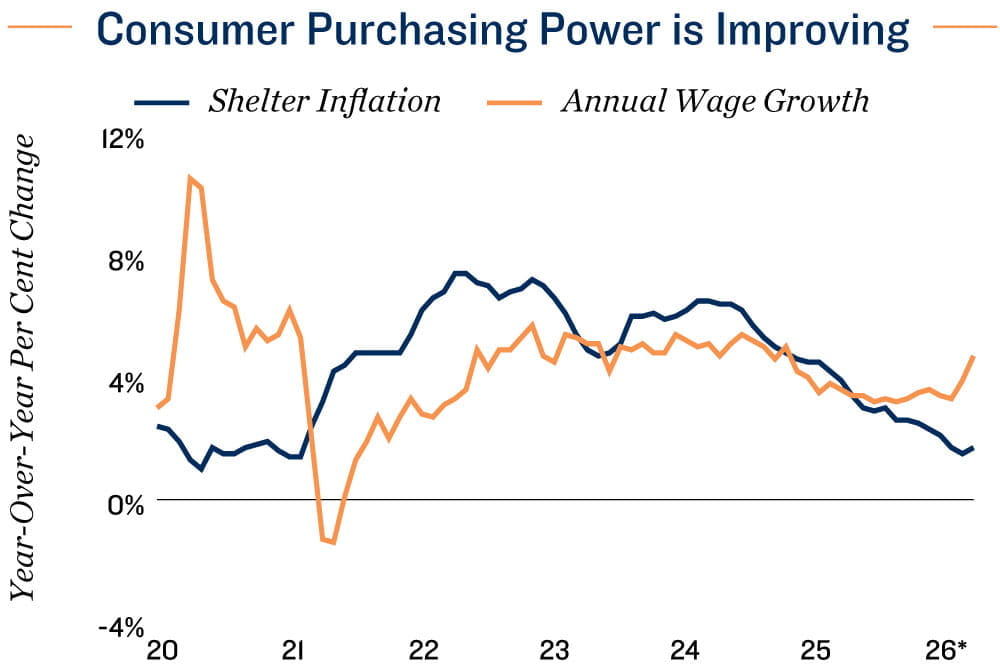

Improving purchasing power aids longer-term demand. While affordability challenges in both the ownership and rental markets continue to weigh on housing demand, household purchasing power has improved. Over the past year, wage growth has generally outpaced shelter inflation, easing some pressure on consumer budgets after several years of rapidly rising costs. This improving income backdrop should gradually support longer-term housing demand, particularly as borrowing costs stabilize. Stronger wage growth could also support broader retail spending. That said, ongoing uncertainty and softer labour market conditions are still likely to keep spending tilted toward essentials-based products until confidence improves further.

* Through March

Sources: Marcus & Millichap Research Services; Altus Data Solutions; Capital Economics; Canadian

Bankers Association; CMHC; CoStar Group, Inc.; Oxford Economics; Statistics Canada

TO READ THE FULL ARTICLE