Research Brief

Interest Rate Outlook

April 2026

What Stabilizing Interest Rates Mean for Commercial Real Estate

Federal Reserve policy remains constrained. Elevated inflation readings and a soft labor market have shifted market expectations toward rates remaining higher for longer.

- Kevin Warsh, President Trump's nominee to succeed Fed Chair Jerome Powell, testified before the Senate Banking Committee, bringing renewed focus on the direction of monetary policy.

- The Fed remains bound by its dual mandate to balance maximum employment with price stability.

- Labor conditions have softened but remain stable, with job growth averaging roughly 22,000 per month over the past year and unemployment in the low- to mid-4 percent band

- An unemployment rate in this range is historically consistent with full employment, limiting the urgency for policy easing.

- Inflation risks have grown, driven largely by rising energy costs, pushing the CPI up 85 basis points last month to 3.3 percent.

- With headline PCE expected to rise toward 3.4 percent, well above the 2 percent target rate, market expectations for near-term rate cuts have diminished sharply

Borrowing costs appear stable. After a brief period of volatility surrounding the Middle East conflict, long-term interest rates have settled for now.

- At the onset of the Iran conflict, the 10-year and 5-year Treasury yields rose roughly 50 basis points, reflecting heightened geopolitical an

- d inflation risk.

- In response to interest rate volatility, CRE lenders widened spreads, temporarily raising the cost of debt capital.

- Treasury yields peaked in late March and have since retreated, with recent movements suggesting rates are stabilizing rather than continuing to trend higher.

- The Blue Chip consensus forecast places the 10-year Treasury near 4.2 percent at year-end, implying a relatively rangebound interest rate environment, barring further shocks.

- Greater stability may support lender confidence, potentially leading to narrower spreads and a lower cost of debt capital.

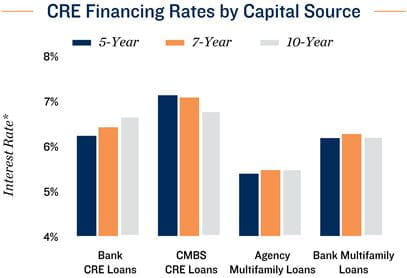

Financing conditions recalibrate. Commercial real estate borrowing costs have returned to a more consistent range across capital sources following early-year disruptions.

- Bank lending for commercial properties is currently consistent with the last quarter of 2025: the low- to mid-6 percent band.

- CMBS borrowing costs remain higher relative to banks, with rates in the 7 percent range.

- Multifamily financing remains comparatively attractive, with agency debt in the low- to mid-5 percent range and bank lending in the low-6 percent range.

- With benchmark rates stabilizing, financing costs appear to have normalized following the early-year disruption.

- Competitive yields, durable cash flows, and inflation-hedging characteristics are increasing CRE's appeal, further reinforced by financial market volatility and rising inflation.

- In a high-inflationary environment, CRE benefits from its role as a hard asset with durable long-term value retention.

| 48% | 25% |

| Pre-Conflict: Chance of 3+ rate cuts by year-end | Current outlook: Chance of 1 rate cut by year-end |

* As of April 13, 2026

Sources: Marcus & Millichap Research Services; Blue Chip Economic Indicators; Board of Governors

of the Federal Reserve; Bureau of Economic Analysis; Bureau of Labor Statistics; CME Group;

Federal Reserve; MMCC

TO READ THE FULL ARTICLE