Research Brief

Employment

April 2026

Focused Job Growth Underpins Broadly Favorable Real Estate Outlook

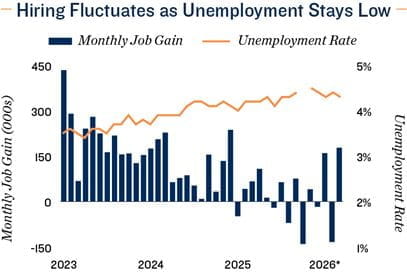

Hiring improved in March. Employers added 178,000 jobs last month, more than offsetting the loss of 133,000 positions in February. Net hiring for the first quarter of 2026 was 205,000, nearly four times that of the same span in 2025. Even so, March’s employment growth was concentrated in only a few sectors, with most new roles tied to health care, dining, construction, and courier services. Outside those industries, job additions totaled about 34,000, while some white-collar fields and the federal government reported contractions.

Office prospects positive despite recent payroll dips. Last month, the number of jobs in information and financial activities fell by 18,000. Professional and business services firms hired only 2,000 workers. Overall, employment in these traditionally office-using industries has fallen about 2 percent since the April 2023 peak, but it is still roughly 4 percent higher than in 2019. The amount of occupied office space, meanwhile, only returned to its year-end 2019 level in December 2025. Growth in the traditional office-using workforce suggests increased demand for space, though the main factor affecting office use remains the shift toward hybrid and in-office schedules. The U.S. office sector enjoyed seven consecutive quarters of positive net absorption through the end of last year, lowering vacancy 90 basis points from a high of 17.2 percent, with more declines expected.

Manufacturing outlook receives boost. The manufacturing sector added 15,000 workers in March, the largest increase since November 2023. Overall, manufacturing employment has fallen by over 300,000 since January 2023. While federal policies have increasingly supported domestic manufacturing, establishing such operations can be slow and require significant capital. Varying tariffs and multiple geopolitical events have created economic uncertainty, making it harder for many firms to commit. Nonetheless, the development of new manufacturing space has been increasing since 2021, with more than 78 million square feet under construction as of April. Semiconductor and battery manufacturing facilities in states like Georgia, Texas, and Ohio lead the pipeline. Vacancy, meanwhile, ended last year in the mid-5 percent zone, over 200 basis points below the overall industrial rate.

Lower in-migration constraining labor force. The unemployment rate dipped 10 basis points to 4.3 percent last month, staying within the same low-to-mid 4 percent band for the past 22 months. March’s decline, however, was driven more by a shrinking labor force than by increased hiring. Lower net international migration has slowed population growth, especially in some of the country’s largest metros, weighing on labor supply and new housing demand.

Interest rate outlook has shifted since February. While the second-best period for job creation in 15 months, after removing walkout effects, mildly eases pressure on the Federal Reserve to lower interest rates, elevated inflation risk from rising oil prices will keep the Fed in a wait-and-see approach. Wall Street participants believe the chances of a cut this year are less than 20 percent. As a result, the 10-year Treasury yield has risen into the mid-4 percent zone. However, this shift is unlikely to stall the upward momentum in investment sales activity that has gathered over the past year, while global uncertainty may steer additional eyes to commercial real estate.

205,000 |

4.3% |

|

Jobs Created Year-to-Date through March 2026 |

Unemployment Rate as of March 2026 |

* Through March

Sources: Marcus & Millichap Research Services; Bureau of Labor Statistics; CME Group; CoStar

Group, Inc.; Federal Reserve; Moody’s Analytics; RealPage, Inc.; U.S. Census Bureau

TO READ THE FULL ARTICLE