Research Brief

Canada Business Outlook Survey

April 2026

Middle East Conflict Pressures Nascent

Recovery in Business Confidence

Confidence turned positive as impact of trade tensions faded. The business sentiment survey indicated a broad‑based improvement in confidence before the ongoing Iran war. Firms have largely looked past trade tensions when assessing future sales, with expectations returning to their historical average. While the USMCA sustains relatively low effective tariff rates on exports to the United States, sup‑ ply‑chain adjustments and greater cost absorption have also helped cushion the impact of trade frictions. Beyond a more constructive sales outlook, investment and hiring intentions strengthened, with the balance of opinion rising above long‑term norms. Progress on trade diversification also continued, as 13 per cent of firms reported growing sales to non‑U.S. markets — up sharply from just 1.0 per cent in the third quarter of 2025. Overall, the firmer business outlook aligns with the recent pickup in economic growth.

Iran war and trade developments add new risks. The fact that most of the survey was conducted before the escalation of the Middle East conflict suggests that these firmer results should be interpreted with caution. In addition, recent signals from the U.S. indicating that the USMCA may not be renewed in its current form could dampen sentiment in the months ahead. A limited follow‑up survey conducted by the Bank of Canada after the outbreak of the Iran conflict shows a more uneven picture: While oil and gas firms expect stronger sales as they maximize use of existing capacity, other businesses anticipate softer demand as higher energy costs strain household budgets and curb discretionary spending.

Commercial Real Estate Outlook

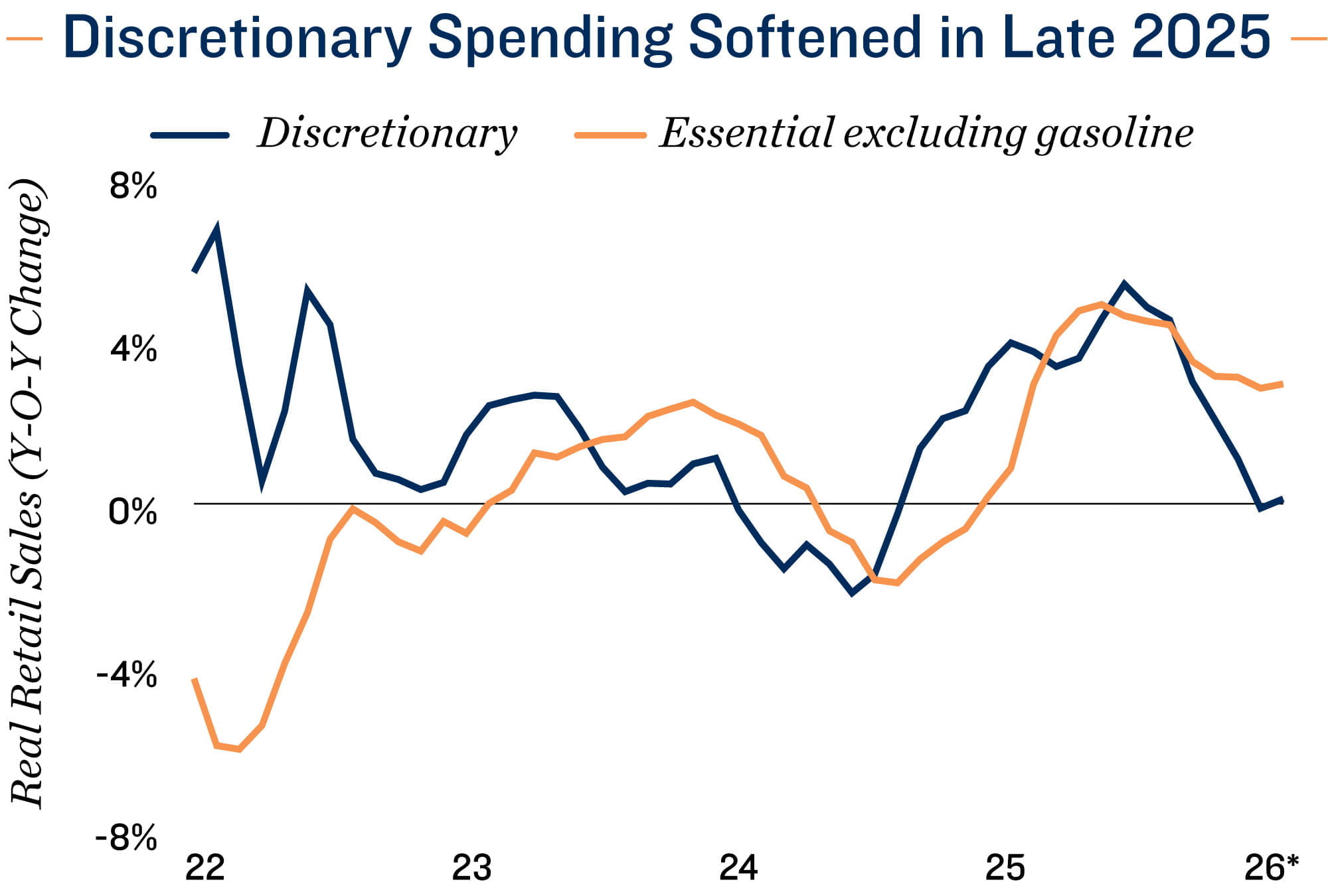

Retailers facing near-term pressures as consumers pull back. Despite the improvement in business sentiment, the latest consum‑ er expectations surveys continue to point to subdued confidence, with the elevated cost of living and a still-soft job market remaining key concerns. Follow‑up surveys conducted amid the ongoing Iran conflict further intensified concerns about gasoline and food prices, as well as broader economic conditions — particularly if the conflict proves prolonged. As a result, the retail sector may face near‑term headwinds. Discretionary retailers appear especially vulnerable, as households rein in nonessential spending amid higher grocery and energy costs and continued labour‑market uncertainty. Coupled with slower population growth, these pressures may reduce retail‑ ers’ appetite for expansion, weighing on leasing momentum in the near term. That said, limited construction expansion should help keep vacancy rates low.

Rising cost pressures weigh on office expansion decisions. For the office sector, the Iran war presents an indirect downside risk through renewed inflationary pressure. A sustained rise in energy prices could keep inflation elevated, limiting further easing by the Bank of Canada and keeping long‑term yields higher for longer. This environment is likely to delay investment plans, particularly in capital‑intensive and growth‑oriented industries such as technology, life sciences, and professional services. As a result, the recovery in office demand may remain uneven in the near term.

* Through January

Sources: Marcus & Millichap Research Services; Bank of Canada; Capital Economics; Oxford

Economics

TO READ THE FULL ARTICLE