Research Brief

Canada Retail Sales

March 2026

Economy Slowing, but Retail Holds Firm Amid

Resilient Demand and Limited Supply

Household consumption gaining momentum. Retail sales rose 1.1 per cent monthly in January, translating into a 1.5 per cent year over year jump. This was an improvement from December’s decline but came in slightly below preliminary expectations. The increase was largely driven by a 2 per cent gain in motor vehicle and parts sales, as activity normalized following seasonal re-tooling shutdowns. Core retail sales — excluding autos and gasoline — also posted a solid 0.9 per cent increase, supported by stronger spending at sporting goods, hobby, and personal care retailers. Meanwhile, gasoline sales edged lower after a strong finish to 2025, and building material sales remained subdued amid persistent winter weather disruptions. Early estimates suggest another 0.9 per cent gain in February, pointing to improved consumer momentum to start the year

Policy outlook is clouded. Despite firmer retail sales in January and a healthy preliminary reading for February, the broader economy remains fragile. While household spending is likely to support modest first-quarter GDP growth, recent indicators — like declining hours worked, weak trade flows and soft manufacturing output — suggest growth will come in below 1 per cent annualized, under the Bank of Canada’s 1.8 per cent forecast. This degree of softness would usually strengthen the case for rate cuts. However, ongoing USMCA renegotiation risks and escalating conflict in the Middle East are adding upward pressure to inflation expectations, creating sufficient uncertainty to keep the central bank on hold through the remainder of the year

Commercial Real Estate Outlook

Population trends impact retail properties. Canada’s population decline in the first quarter of 2026 introduces an additional headwind for retail sales and broader sector performance. Slower population gains reduces the pace of aggregate consumption, contributing to a modest softening in retail property fundamentals, with the national vacancy rate to rise for a third consecutive year to just below 3 per cent. That said, the composition of demand is shifting. In recent years, retail sales growth was driven by rapid population gains, masking soft per capita spending amid higher interest rates. Now, with population growth slowing and borrowing costs easing, consumption is being supported more by spending per person, partially offsetting the drag on overall sales volumes. Meanwhile, with population growth forecast to return to historic levels by 2028, Canada’s retail property sector continues to hold a sound outlook, supporting investor confidence.

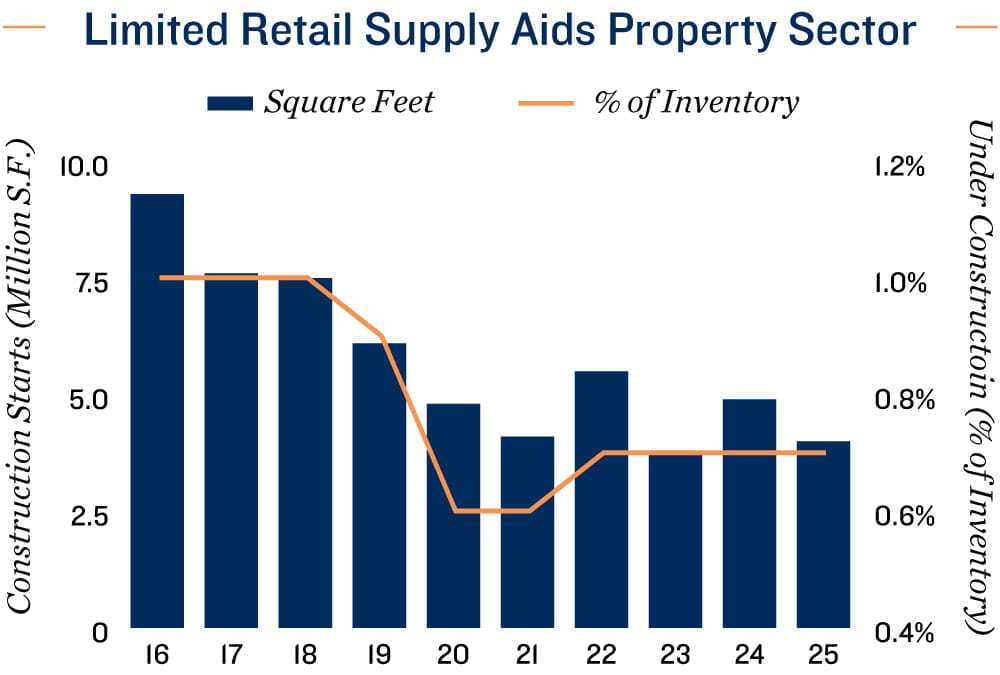

Tight build pipeline reinforces stability. Limited supply continues to underpin an optimistic outlook for retail property performance. Development has been on a downward trend for the past decade, as e-commerce, pandemic uncertainty and elevated construction costs curtailed projects. More recently, a slowdown in mixed-use development tied to weaker residential construction has further limited space additions, with starts in 2025 down nearly 60 per cent compared to 2016. As population growth returns to more sustainable long-term averages in the coming years, these constrained supply conditions are expected to help stabilize vacancy at a tight level of roughly 3 per cent by the end of next year, reinforcing the sector’s underlying resilience.

* Forecast provided by Oxford Economics

Sources: Marcus & Millichap Research Services; Altus Data Solutions; Capital Economics; CMHC;

CoStar Group, Inc.; Oxford Economics; Statistics Canada

TO READ THE FULL ARTICLE