Research Brief

Canada Housing

January 2026

Residential Markets Beginning to Adjust

as Economic Visibility Improves

Canada’s housing market closed out 2025 on a softer note. National home sales fell 2.7 per cent monthly in December, while full-year transactions were down 1.9 per cent from 2024, closing out an uneven year defined by uncertainty and shifting buyer confidence. Activity was subdued early in the year as tariff risks sidelined buyers, before rebounding through the spring and summer on pent-up demand and improving financing conditions. That momentum faded toward yearend, with December’s pullback driven by slowdowns in several major markets. Pricing also softened modestly, as the median single-family home price declined 0.2 per cent monthly, translating into a 3.6 per cent year-over-year drop. That said, overall conditions remained balanced with the sales-to-new listings ratio at 52.3 per cent amid restrained new supply and inventories below long-term norms.

A brighter future could materialize. Canada’s housing market is expected to improve modestly in 2026, supported by a more predictable lending environment that should gradually draw buyers back into the market. With borrowing costs now viewed as stable and major financial institutions forecasting limited rate volatility, improved financing visibility is expected to lift confidence and unlock some pent-up demand. While mortgage rates are likely to remain above recent norms, reduced uncertainty should support a gradual rebound in sales, particularly through the spring market. Price growth is expected to remain measured, constrained by affordability pressures. Still, firmer demand and limited supply in many regions could help stabilize values and support modest gains over the course of the year.

Commercial Real Estate Outlook

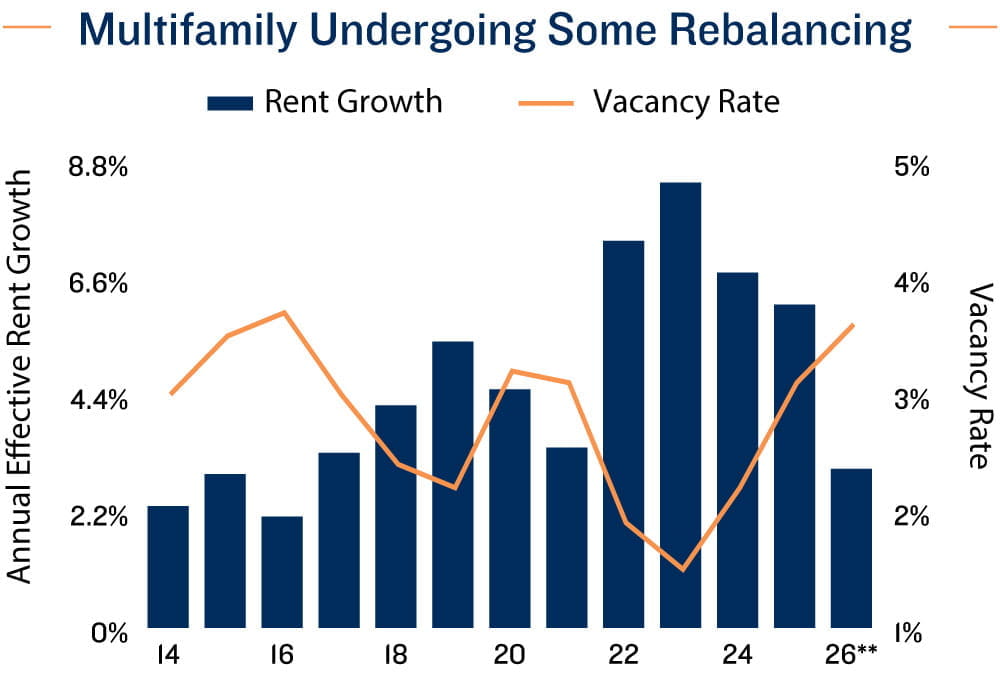

Balance returning to residential markets. Canada’s multifamily sector entered 2026 with healthy fundamentals that are normalizing after an exceptionally tight cycle. In 2025, apartment vacancy rose 90 basis points to 3.1 per cent, while annual rent growth moderated 60 basis points to 6.1 per cent, reflecting evolving supply-demand dynamics. Vacancy is expected to climb further into the 3.5 per cent range this year, with rent growth continuing to moderate. This is being driven primarily by elevated openings, as purpose-built rental completions remain high and investor-owned condos continue to flow into the rental pool. Meanwhile, tighter immigration is pushing population growth toward zero. These dynamics are likely to continue to place upward pressure on vacancy and cap rent growth over the short to medium term. That said, underlying conditions remain strong, supporting stable and reliable long-term cash flow.

Sales momentum could grow. Over the past year ended September, roughly 1,480 apartment buildings sold, with dollar volume of $9.6 billion, down from $10.9 billion in 2024. The slowdown was most pronounced among larger deals, as sales over $20 million declined in both count and value, reflecting bid-ask spreads, tighter underwriting, and cautious institutional capital. Midsize and smaller deals continued to drive activity, highlighting the role of private and domestic capital in maintaining liquidity. While activity was well below cycle highs, preliminary estimates for full-year sales suggest the market is shifting from price discovery to an early-stage recovery amid stabilizing income growth and improving financing conditions

* Forecast through 2027; ** Forecast

Sources: Marcus & Millichap Research Services; Altus Data Solutions; Canada Mortgage and

Housing Corporation; Capital Economics; CoStar Group, Inc.; Statistics Canada

TO READ THE FULL ARTICLE