Research Brief

Canada Industrial

December 2025

National Strategy Bolsters Long-Term Outlook Despite New Trade Barriers

New tariffs disrupt manufacturing recovery. After four consecutive months of improvement, Canada’s manufacturing sales increased at a slower annual pace, weighed down by shipments falling 1.0 per cent in October. The sector faced a renewed shock as the United States imposed tariffs on softwood lumber, resulting in a 9.0 per cent monthly drop in wood product shipments. Transportation equipment sales also fell, down 2.3 per cent, driven by weaker production of aerospace products and parts. Looking ahead, shipments in the transportation equipment sector could remain under pressure entering 2026, as new U.S. tariffs of 25 per cent on medium- and heavy-duty trucks and 10 per cent on buses took effect in November. Moreover, ongoing efforts by several automakers to move parts of production capacity south of the border could further strain the sector, affecting overall sales in the short term.

Beyond tariffs, trade strategy points to long-term upside. Despite the newly implemented tariffs, Canada still benefits from its existing trade agreements, with about 90 per cent of exports entering the United States duty-free. While trade negotiations appear to have stalled, the upcoming 2026 joint review of the USMCA could provide renewed momentum for the ongoing manufacturing recovery. Looking past short-term trade policy uncertainty, Canada’s long-term plan to diversify trade aims to double exports of goods and services to non-U.S. markets over the next decade. This could support longer-term growth in the nation’s manufacturing sector.

Interest rate clarity to help restore tenant confidence. October’s drop in manufacturing sales, coupled with a lower-than-expected inflation reading for November, likely strengthened the Bank of Canada’s view that the current policy rate is broadly appropriate to keep inflation at target while supporting the economy through an ongoing structural adjustment. This greater clarity on interest rates is expected to support leasing activity in the industrial sector. With more predictable financing conditions, tenants needing capital outlays for facility improvements and customized build-outs should find it easier to budget for and implement these investments. Additionally, clearer signals that rates have stabilized will allow tenants to better forecast operating costs and proceed with space decisions that were previously delayed

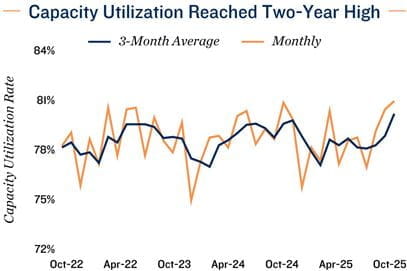

Firms operating at relatively high capacity. Even as total manufacturing sales declined, the manufacturing capacity utilization rate rose to 80.7 per cent — its highest level since March 2022 — driven by gains in the food, petroleum and coal subsectors. This divergence suggests that manufacturers were operating closer to their maximum output, potentially rebuilding inventories or preparing for future demand despite softer current sales. If this momentum continues, manufacturers may find it more compelling to seek additional or larger industrial space to meet production needs. This could provide a supportive backdrop for leasing activity in the industrial sector entering the new year.

Sources: Marcus & Millichap Research Services; Altus Data Solutions; Statistics Canada

TO READ THE FULL ARTICLE