Research Brief

Inflation

April 2024

Unexpected Jump in Prices May Push Rate Cut Timeline

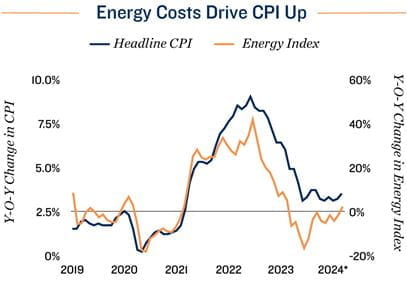

Energy cost spike bumps up inflation. Mounting costs for gasoline and electricity kept overall inflation elevated over the 12-month period ending in March. The headline CPI measure grew by 3.5 percent during the span, ticking up as the energy index moved into positive territory for the first time since February 2023. Geopolitical conflict, spring-season travel, and energy providers shifting operations amid warmer weather contributed to these higher costs. Fortunately, the seasonality of rising energy prices suggests that such inflationary pressures should stabilize over the short-term.

Cooling grocery prices could benefit shopping center foot traffic. While energy costs rose unexpectedly, other necessities are noting substantially cooler pricing pressures. The index for personal care moderated to its lowest pace in 26 months through the yearlong span ending in March, while the groceries index — at just 1.2 percent year-over-year — was only a fraction of the 13.5 percent peak noted in August 2022. Recent disinflation for personal care items and groceries is taking some burden off consumers who prioritize such goods, which, in turn, has supported exceptional performance at supermarkets as of late. Segment vacancy remained below 3.0 percent in the first quarter of 2024, much lower than the broader retail sector's, while the average asking rent for these properties elevated above $14 per square foot — the highest level in over a decade.

Cooling grocery prices could benefit shopping center foot traffic. While energy costs rose unexpectedly, other necessities are noting substantially cooler pricing pressures. The index for personal care moderated to its lowest pace in 26 months through the yearlong span ending in March, while the groceries index — at just 1.2 percent year-over-year — was only a fraction of the 13.5 percent peak noted in August 2022. Recent disinflation for personal care items and groceries is taking some burden off consumers who prioritize such goods, which, in turn, has supported exceptional performance at supermarkets as of late. Segment vacancy remained below 3.0 percent in the first quarter of 2024, much lower than the broader retail sector's, while the average asking rent for these properties elevated above $14 per square foot — the highest level in over a decade.

Slower apartment rent growth keeps core inflation down. Stripping out the impacts from the food and energy indices, core CPI rose 3.8 percent over the year ending in March — tied for the lowest reading since May 2021. Cooling expenses for housing services are primarily keeping core inflation on a downward path, with annual growth in the rent index tapering by over 300 basis points from May 2023. During that time, the percentage of U.S. apartments offering concessions grew by more than 500 basis points, as many operators looked to safeguard occupancy amid record-level new supply. Completions are expected to elevate even more this year, potentially motivating operators of newer apartments to further lean on concessions. The national average effective apartment rent is expected to grow by 1.5 percent in 2024, below the trailing decade-long average of 5.4 percent. While temporarily leading apartment investors to re-tool their short-term strategies, cooler rents will be vital to keeping core inflation down.

Fed cuts may be delayed. Bumpier CPI inflation has pushed back Wall Street expectations for the Federal Reserve to begin cutting interest rates from June to September. Still, the Fed tracks Core PCE more closely, which places lower weights on several CPI components, including housing costs. Core PCE has been on a cooling trend, and a lower March reading — set to be released on April 26 — could sway Fed expectations again. If Core PCE continues to come down, after already reaching 2.8 percent in February, this month's elevated CPI measure may be less impactful on the Fed's decision-making process.

Lending spreads remain narrow. The yield on a 10-year treasury reached a 21-week high after the CPI data release, amid reduced demand for treasuries and higher-for-longer interest rate expectations. Elevation in the 10-year yield is keeping lenders' spreads narrower than historical norms, reducing the pool of investment opportunities deemed viable for financing. However, should multiple cuts occur this year, lenders and borrowers will be better-positioned to pin down terms. Financing uncertainty — which has challenged deal flow since mid-2022 — will gradually alleviate, helping revive trading activity.

3.5% |

3.8% |

|

Increase in Headline CPI Year-Over-Year |

Increase in Core CPI Year-Over-Year |

* Through March

Sources: Marcus & Millichap Research Services; Bureau of Labor Statistics; CME Group; Federal Reserve;

RealPage, Inc.; Census Bureau; Bureau of Economic Analysis; CoStar Group, Inc.; TSA

TO READ THE FULL ARTICLE