Research Brief

Canada Monetary Policy

April 2024

Central Bank Maintains Overnight Rate,

While Turning Slightly More Dovish

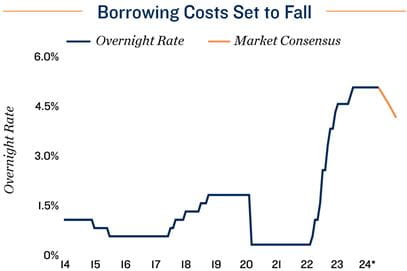

Central Bank holds policy rate for sixth consecutive meeting. The Bank of Canada left its policy rate unchanged at 5.0 per cent in April, a move widely anticipated among economists and investors. While inflation has fallen by more than expected over the past two months and the unemployment rate hit a 26-month high in March, Canada’s Central Bank still believes risks remain and wants to see further evidence that underlying inflationary pressures are continuing to moderate. The BoC cited shelter inflation as one of its main concerns. However, the Bank also stated that while inflation is still too high, the three-month annualized rate of core inflation suggests further easing ahead, and that the monetary authority is beginning to see what is needed in order to bring inflation back to the Bank’s target. A mid-year rate cut still holds as a likely outcome.

Money markets lower probability of June rate cut. The BoC turned more dovish by stating that easing price pressures are becoming more broad-based, and recent data has increased their confidence that inflation will continue to trend down. The Central Bank also noted they believe economic growth will pick up over the course of 2024, largely due to strong population growth and a recovery in household spending. While this was not an outright signal to the economy, consumers will need to see some relief in the form of lower borrowing costs for this to happen. Despite this, interest rate swap markets lowered the probability of a June interest rate cut from roughly 70 per cent prior to the announcement to just under 60 per cent. This can mainly be attributed to inflation warnings in the U.S. and strong Canadian economic growth to start 2024.

Commercial Real Estate Outlook

Commercial real estate investment activity gaining momentum. While the timing and depth of interest rate cuts still remains a mystery among commercial real estate investors, the direction in which borrowing costs are headed has never been more clear. As a result, investor confidence has gradually been growing since the third quarter of last year as uncertainty has begun to abate, helping to slowly narrow price expectation gaps between many buyers and sellers. This growing confidence has been reflected in commercial real estate sales activity. Over the final three months of last year, total dollar volume transacted increased 5.0 per cent quarterly, translating into a 10 per cent year-over-year gain. Looking ahead, this trend is likely to continue — especially for preferred assets like anchor-based retail and industrial — as these property types generally offer more liquidity and have greater access to financing.

Housing affordability a major concern. The current environment of elevated borrowing costs has put a strain on housing affordability. While rising interest rates over the past two years have caused the median price of a single-family home to fall roughly 15 per cent from the February 2022 peak, heightened financing costs have had a greater impact on overall affordability. Canada’s housing affordability index — which is the ratio of housing-related costs to average household disposable income — was at its highest level on record as of the end of 2023. Looking ahead, affordability challenges are likely to grow. The combination of historic population growth and declining housing starts in 2023 suggest Canada’s housing supply-demand gap will widen, driving the need for more housing stock nationwide.

* Market consensus an average of forecasts from TD, RBC, BMO, CIBC, Scotiabank

Sources: Marcus & Millichap Research Services; Altus Data Solutions; Bank of Canada;

Canada Mortgage and Housing Corporation; Capital Economics; CoStar Group, Inc.; Statistics Canada

TO READ THE FULL ARTICLE